FAQ: What benefits leaders need to know about fertility mandates

The landscape is moving fast. Here are the questions benefits leaders are asking about IVF and fertility benefits — and the answers that will help you stay ahead.

Fertility benefits used to be a talent differentiator. Now they're a benefit, a compliance question, and an increasingly urgent line item on the CFO's radar. With federal proposals advancing and more than half of U.S. states introducing or carrying over fertility legislation in 2026, the landscape has changed — and so has what benefits leaders need to know. Whether you're trying to understand your mandate exposure, benchmark your current benefit, or make the case internally for better coverage, this is the resource to start with.

Which states require employers to cover IVF right now?

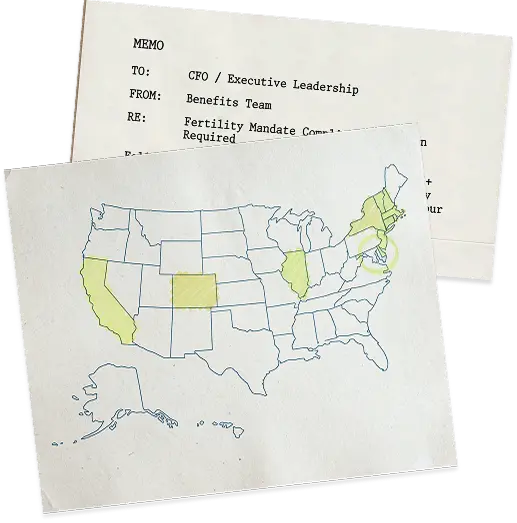

1. Which states require employers to cover IVF right now?

Twenty-five states and Washington, D.C. currently have laws requiring some form of private insurance coverage for fertility care, as of July, 2026 — but requirements vary widely across what's covered (IVF, IUI, medications, preservation), who qualifies, and which plan types are affected.

States with the most comprehensive IVF mandates include

Several others — including Georgia, Florida, Nevada, and Virginia — have recently passed more targeted laws covering fertility preservation for cancer patients or codifying the right to access IVF without mandating insurance coverage.

Explore our interactive map for up-to-date information, no matter where you and your employees are located.

Do state mandates apply if we're self-insured?

2. Do state mandates apply if we're self-insured?

For most large employers, the answer is no.

State mandates generally apply to fully insured plans — where you buy coverage from an insurance carrier that is regulated by your state. If your plan is self-insured, federal ERISA law governs it instead, and ERISA generally preempts state insurance regulations.

In practice, this means a self-insured employer headquartered in California or New York is generally not required to cover IVF as part of these state insurance mandates. But their fully insured competitors in those same states are — and as more states adopt mandates (over half introduced or carried fertility legislation in 2026), covering IVF is quickly becoming the market norm in those states, not the exception. Self-insured employers who treat their ERISA exemption as a permanent advantage are increasingly competing for talent against companies that are legally required to offer it. Most large employers are self-insured, so this distinction affects the majority of enterprise benefits leaders.

Where does federal IVF policy stand right now?

3. Where does federal IVF policy stand right now?

There are several active proposals, but nothing has passed into law yet. Here's the current status of the four most significant federal developments:

- Executive Order: Expanding Access to In Vitro Fertilization (signed February 2025): This order directed federal agencies to develop proposals for protecting IVF access and reducing out-of-pocket costs. This has already influenced how the administration talks about fertility care — as a medical necessity rather than an elective procedure. Regulatory guidance stemming from this order is still being developed, including a proposed "Excepted Fertility Benefits" rule that would let employers offer fertility coverage as a standalone "excepted benefit" outside standard ACA requirements — but with a $120,000 lifetime cap on covered benefits. The public comment period on this proposal closed July 13, 2026; final rulemaking has not been issued.

Maven submitted a public comment on the proposal, recommending the rule allow cycle-based limits as an alternative to a flat dollar cap — consistent with our broader position (see Q6) that cycle caps are easier for members to plan around and less likely to cut off treatment mid-cycle than a hard dollar ceiling. - Proposed Rule on Fertility Excepted Benefits (issued May 2026): The Departments of HHS, Labor, and Treasury recently released a proposed rule that would enable employers to offer fertility benefits as a new category of limited excepted benefits—separate from their primary group health plan—provided that substantially all benefits are for the diagnosis, mitigation, or treatment of infertility or related reproductive health conditions; that benefits are subject to a combined lifetime maximum; and that participants receive a required notice describing the coverage. Maven submitted a public comment supporting the proposed rule, which would establish a streamlined pathway for employers to offer standalone fertility benefits without the regulatory complexity and costs associated with traditional group health plan coverage.

- The Protect IVF Act (S.2035, introduced June 2025): This would give providers the legal right to offer fertility treatment, patients the right to receive it, and insurers the right to cover it — without interference. This is currently sitting in the Senate HELP Committee, but has not advanced to a floor vote.

- The Health Coverage for IVF Act (H.R.3480, introduced May 2025): This would add fertility treatment to the ACA's list of essential health benefits, effectively requiring all ACA-compliant plans to cover it nationwide — including individual and small group markets that state mandates don't currently reach. This is also in committee with no vote currently scheduled.

What does a well-designed employer IVF benefit actually include?

4. What does a well-designed employer IVF benefit actually include?

A complete fertility benefit covers diagnostics (bloodwork, hormone panels, semen analysis), medications, IVF procedures, genetic testing (PGT), embryo transfers, and cryopreservation and storage. It should also include fertility preservation for employees undergoing cancer treatment, plus structured trying-to-conceive (TTC) coaching and guidance, care navigation, and mental health support — all of which meaningfully improve clinical outcomes, engagement, and cost.

Plans that cover procedures but not medications, or cycles but not storage, leave employees absorbing the difference out of pocket — and often delay or abandon treatment as a result.

Maven covers all of this within a single managed benefit. More than 40% of Maven fertility members access mental health coaching during treatment, and Care Advocates are available within an hour on average to help members navigate next steps, find in-network providers, and stay on track.

What are the most important plan design decisions employers make?

5. What are the most important plan design decisions employers make?

Four decisions shape most of the cost and outcome variation in fertility benefits:

- Cycle caps vs. dollar limits [cycle caps limit the number of treatment rounds covered; dollar limits set a maximum spend]: Cycle caps are often easier for members to plan around.

- Step therapy [a protocol requiring employees to try less intensive treatments before IVF is authorized]: Requiring IUI before IVF authorization sounds like a cost-saver, but poorly designed protocols often delay effective treatment and increase total spend.

- Centers of Excellence [a network of credentialed fertility clinics selected for quality, outcomes, and cost-effectiveness]: Directing members to credentialed clinics with strong outcome data is one of the most effective ways to manage cost and improve results.

- Inclusive eligibility [the criteria determining who qualifies for fertility benefits under your plan]: Benefits that require a formal infertility diagnosis or restrict access based on relationship status or sexual orientation are increasingly out of step with both workforce demographics and state law.

What fertility treatments are actually required under state mandates — and what's excluded?

6. What fertility treatments are actually required under state mandates — and what's excluded?

What's commonly required: infertility diagnosis, IUI, IVF procedures, and fertility preservation for cancer patients. What's frequently excluded: preimplantation genetic testing, donor eggs or sperm, embryo storage beyond a short initial window, and surrogacy-related costs.

Access for LGBTQ+ individuals and single employees also varies significantly by state. Older mandates often required a heterosexual couple with a documented infertility diagnosis. Newer laws — including California's SB 729 — explicitly extend coverage regardless of sex, relationship status, or prior diagnosis.

Are employers in non-mandate states offering IVF benefits anyway?

7. Are employers in non-mandate states offering IVF benefits anyway?

Yes — and the primary driver is employee health outcomes. Without employer coverage, employees in non-mandate states are more likely to delay or forgo treatment, attempt riskier protocols to reduce costs, or transfer multiple embryos to avoid paying for additional cycles — all of which increase the likelihood of complications, high-risk pregnancies, and NICU admissions.

Unmanaged fertility care is expensive care. Nationally, IVF miscarriage rates run 18–30%, according to the SART National Summary Report, and 12.5% of IVF births result in multiples, according to the CDC National ART Surveillance — a key driver of NICU admissions and employer cost. In contrast, Maven members experience an 11% miscarriage rate, a 98% singleton rate, and a 1.8% multiples rate. And 30% of Maven fertility members never need IVF or IUI at all. Those outcomes are the direct result of clinical governance and early intervention, not geography.

How do you offer a strong fertility benefit without breaking the budget?

8. How do you offer a strong fertility benefit without breaking the budget?

Clinical management, not benefit restriction. Cutting cycles or adding barriers reduces access but doesn't address what actually drives cost: unmanaged utilization, preventable complications, and treatment that starts too late.

Most fertility cost problems aren't a coverage problem — they're a management problem. The most effective approach combines three things: Centers of Excellence to reduce unnecessary interventions and drive better clinical outcomes; evidence-based protocols that limit add-ons that increase cost without improving results; and preconception support, which is where the biggest cost avoidance happens. 30% of Maven fertility members achieve pregnancy without IVF or IUI at all, and members who participate in fertility coaching are 55% more likely to conceive without treatment. Every member who conceives without a procedure is a cycle that was never needed.

How do we know a fully integrated benefit actually pays for itself?

9. How do we know a fully integrated benefit actually pays for itself?

Because the cost drivers are measurable — and so are the reductions.

The average unmanaged pregnancy costs $50,000+. A NICU admission can exceed $100,000. C-sections cost roughly 50% more than vaginal deliveries and carry a longer recovery tail. These are predictable, recurring costs that compound when care is fragmented and no one is accountable for what happens between benefit touchpoints.

An integrated benefit changes the math by intervening earlier and maintaining clinical continuity across the full journey, and the outcomes are claims-validated. The question isn't whether an integrated benefit costs more than a point solution.

- 27% lower NICU admission rate among Maven members — one avoided admission can offset a year of program costs

- Lower C-section rates — reducing one of the most consistent drivers of elevated maternity spend

- $9,600 saved per birth — a figure derived from early intervention and continuity of care, not benefit design alone

- 2.6x–5.1x estimated clinical and business ROI across the full program

Leading employers aren't waiting for a federal mandate to land. See how they're designing fertility benefits now — and what that could mean for your organization.